How to Get Life Insurance in 2024 | An Affordable Insuance?

Life insurance is a crucial component of financial planning that often gets overlooked. It provides a safety net for your loved ones in the event of your untimely demise, offering financial support when they need it the most. In this guide, we will explore the ins and outs of obtaining life insurance, helping you make informed decisions to safeguard your family’s future.

Life insurance is more than just a financial product; it’s a proactive step towards ensuring the well-being of your family in the face of uncertainties. Many individuals delay or avoid the process due to a lack of understanding or misconceptions. However, the peace of mind and financial security it provides make the effort worthwhile.

Contents

- 1 How to Get Life Insurance

- 2 Understanding Life Insurance

- 3 Assessing Your Needs

- 4 Choosing the Right Policy

- 5 Application Process

- 6 Common Mistakes to Avoid

- 7 Understanding Premiums and Payments

- 8 Dealing with Pre-existing Conditions

- 9 Policy Riders and Add-ons

- 10 Life Insurance and Financial Planning

- 11 FAQs

- 12 Conclusion

How to Get Life Insurance

To obtain life insurance, the process typically involves several key steps. Firstly, it’s essential to assess your insurance needs and determine the coverage amount that suits your financial goals and responsibilities. Next, research and compare different insurance policies offered by various providers to find the one that aligns with your requirements and budget.

After submitting your application and completing any necessary medical exams, the insurance company will review your information and determine your premium rate. If approved, you’ll receive a policy document outlining the terms and conditions of your coverage. Insurance companies may require a medical examination as part of the underwriting process to assess.

Keep in mind that it’s crucial to be honest and accurate in your application to ensure the policy’s validity. Seeking guidance from insurance professionals or financial advisors can also help you navigate the complexities of choosing the right life insurance policy for your specific needs.

Understanding Life Insurance

Life insurance is a financial tool designed to provide a financial safety net for loved ones in the event of the policyholder’s death. There are several types of insurance, with the two main categories being term life and permanent insurance. Term life offers coverage for a specified term, providing a death benefit if the insured passes away during that period. Permanent insurance, on the other hand, covers the policyholder for their entire life and includes a cash value component that can accumulate over time.

Premiums, the payments made for life insurance coverage, are influenced by factors such as age, health, and the chosen coverage amount. Understanding the purpose of insurance is crucial; it helps protect dependents from financial hardship, covering expenses like mortgage payments, education costs, and daily living expenses. It’s essential to regularly review and update insurance coverage to align with changing financial circumstances, ensuring that the policy continues to meet the needs of the insured and their beneficiaries.

Assessing Your Needs

Assessing your life insurance needs is a vital step in securing financial protection for your loved ones. Start by evaluating your financial obligations, such as outstanding debts, mortgage payments, and educational expenses for dependents. Consider your income and how it contributes to your family’s financial well-being.

Factor in your current and future expenses, including funeral costs and potential estate taxes. Additionally, assess your spouse’s income, existing savings, and any other sources of financial support available to your family.

Your health and age also play a crucial role in determining the appropriate coverage. Younger, healthier individuals may opt for term life insurance, providing coverage for a specific duration. Those seeking long-term protection and potential cash value accumulation may consider permanent life insurance.

Regularly review and adjust your life insurance coverage as your circumstances change, such as marriage, the birth of children, or career advancements. Consulting with financial advisors can help you make informed decisions tailored to your unique situation, ensuring that your life insurance adequately addresses your evolving needs.

Choosing the Right Policy

When selecting the right life insurance policy, consider the following key points:

- Assess Your Needs: Identify your financial obligations, including debts, mortgage, and future expenses like education or funeral costs.

- Term vs. Permanent: Decide between term life insurance for a specific duration and permanent life insurance, which covers your entire life and may accumulate cash value.

- Premiums and Affordability: Understand how premiums are calculated based on factors like age, health, and coverage amount. Ensure the chosen policy fits your budget.

- Coverage Amount: Determine an appropriate coverage amount that adequately protects your loved ones in the event of your death.

- Health Evaluation: Be prepared for a health evaluation, as your health influences the cost and availability of life insurance.

- Review Periodically: Regularly reassess your life insurance needs with life changes, such as marriage, childbirth, or career advancements, and adjust your policy accordingly.

- Seek Professional Advice: Consult financial advisors or insurance professionals to navigate policy options and make well-informed decisions aligned with your specific circumstances.

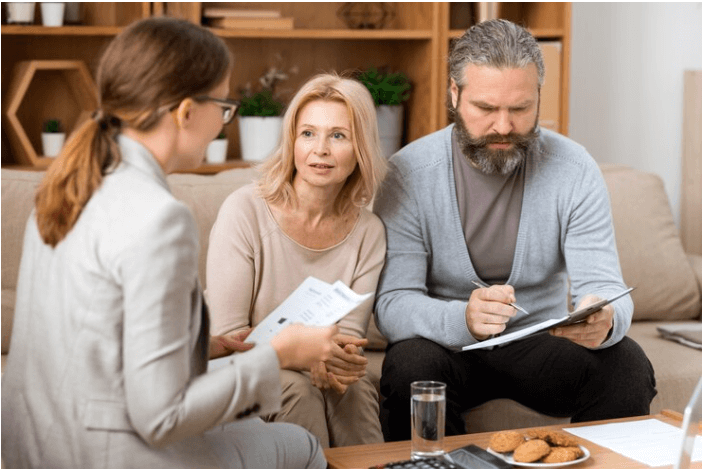

Application Process

The life insurance application process involves several steps:

- Needs Assessment: Evaluate your financial obligations and determine the coverage amount required to protect your loved ones adequately.

- Research Policies: Explore different life insurance policies, considering factors like term or permanent coverage, premiums, and benefits.

- Application Submission: Complete the application form, providing accurate information about your health, lifestyle, and medical history.

- Medical Examination: Some policies may require a medical exam to assess your health, helping the insurance company determine the risk associated with insuring you.

- Underwriting: The insurance company reviews your application, medical exam results, and other relevant information to determine your eligibility and premium rate.

- Policy Approval: If approved, you’ll receive a policy document outlining the terms and conditions of your coverage.

- Premium Payment: Once approved, start paying your premiums as outlined in the policy to keep the coverage active.

- Policy Delivery: The insurance company provides you with the finalized policy documents for your records.

Throughout the process, honesty and accuracy are crucial to ensure the validity of the policy. Seeking guidance from insurance professionals can help navigate complexities and make informed decisions.

Common Mistakes to Avoid

When purchasing life insurance, it’s crucial to avoid common mistakes that can impact the effectiveness of your coverage. One frequent error is underestimating coverage needs. Failing to account for essential expenses, such as outstanding debts, mortgage payments, and educational costs, may leave loved ones financially vulnerable. Additionally, overlooking the importance of regular policy reviews can result in outdated coverage that no longer aligns with changing circumstances.

Another common mistake is providing inaccurate information during the application process. Being dishonest about health conditions or lifestyle factors can lead to denied claims or policy cancellations. Neglecting to consider the long-term implications of the chosen policy type is also a pitfall. While term life insurance may be suitable for some, others may benefit more from the permanence and potential cash value of a permanent life insurance policy.

Understanding Premiums and Payments

Premiums for life insurance are calculated based on factors like age, health, and coverage amount. Payment frequency options include monthly, quarterly, semi-annually, or annually, each with its financial implications. Common payment methods include electronic funds transfer, credit/debit cards, or checks. Timely and regular premium payments are crucial to maintaining an active policy, and understanding these elements ensures a well-managed life insurance plan.

Premiums for life insurance are calculated based on various factors that influence the risk the insurance company assumes by covering an individual. These factors typically include age, health status, lifestyle choices, occupation, and the chosen coverage amount. Younger, healthier individuals usually pay lower premiums as they pose a lower risk to the insurer. Additionally, the type of policy, whether term or permanent life insurance, and any riders or additional features selected can also impact premium costs. Generally, term life insurance tends to have lower premiums than permanent life insurance.

Premium payments can be made through various frequencies and methods, providing flexibility for policyholders. Common premium payment frequencies include monthly, quarterly, semi-annually, or annually. Monthly payments may be convenient but can result in slightly higher overall costs due to processing fees. Annual payments, on the other hand, often come with discounts.

Dealing with Pre-existing Conditions

Addressing pre-existing conditions is a crucial aspect of obtaining life insurance. While pre-existing health conditions can impact premium rates and eligibility, it’s essential to be transparent during the application process. Providing accurate information allows the insurance company to assess the risk accurately, ensuring the policy remains valid.

Shopping around and consulting with different insurance providers is advisable to find the most favorable terms for your situation. Some insurers specialize in covering individuals with specific health conditions and may offer more competitive rates. Individuals with pre-existing conditions may face higher premiums, and in some cases, the insurer may impose exclusions or limitations.

In certain instances, individuals may be eligible for a graded or modified benefit policy, providing coverage with certain limitations initially, which may be lifted or expanded over time. Seeking guidance from insurance professionals can help navigate the complexities of obtaining life insurance with pre-existing conditions and ensure that you find the best possible coverage for your needs.

Policy Riders and Add-ons

Policy riders and add-ons offer individuals the opportunity to customize their life insurance coverage to better suit their unique needs. These optional enhancements can provide additional benefits beyond the standard policy. Common riders include:

- Critical Illness Rider: Provides a lump-sum payment upon diagnosis of a covered critical illness, offering financial support for medical expenses.

- Accidental Death Benefit Rider: Offers an additional payout if the insured’s death results from an accident, supplementing the standard death benefit.

- Waiver of Premium Rider: Waives future premium payments if the insured becomes disabled, ensuring continued coverage during challenging times.

- Accelerated Death Benefit Rider: Allows the policyholder to receive a portion of the death benefit if diagnosed with a terminal illness, offering financial assistance for medical costs.

- Child Rider: Extends coverage to children, providing a death benefit if the child passes away, and may also include options to convert to a separate policy in the future.

Selecting riders depends on individual circumstances and priorities, providing flexibility to tailor the policy to specific needs. However, it’s essential to carefully evaluate the costs and benefits of each rider to ensure they align with your overall life insurance strategy.

Life Insurance and Financial Planning

Life insurance plays a pivotal role in comprehensive financial planning, providing a crucial safety net for loved ones in the event of the policyholder’s death. It serves as a financial cushion, helping to cover outstanding debts, mortgage payments, and other essential expenses. The death benefit paid to beneficiaries can offer financial stability, allowing them to maintain their standard of living.

Life insurance is particularly important during key life stages, such as marriage, parenthood, or homeownership, where financial responsibilities increase. It acts as a strategic tool in wealth transfer, estate planning, and ensuring the continuity of business operations.

FAQs

How can I get my own life insurance?

To get your own life insurance, assess your needs, research policies, and choose a coverage type. Complete an application, that provides accurate health and lifestyle information. Some policies may require a medical exam. Once approved, pay premiums to keep the coverage active.

How do you receive life insurance?

In most cases, your beneficiary will receive a check in the mail for the lump-sum amount of the death benefit, unless the beneficiary indicates that he or she wants the money converted into an annuity (which pays a specified sum every year).

How much money do you need for life insurance?

Most insurance companies say a reasonable amount for life insurance is at least 10 times the amount of annual salary. If you multiply an annual salary of $50,000 by 10, for instance, you’d opt for $500,000 in coverage. Some recommend adding an additional $100,000 in coverage per child above the 10x amount.

What makes you get life insurance?

Buying life insurance protects your spouse and children from the potentially devastating financial losses that could result if something happened to you. It provides financial security, helps to pay off debts, helps to pay living expenses, and helps to pay any medical or final expenses.

Does life insurance give money?

Depending on the insurer, a life insurance payout can typically be distributed in three ways: in the form of a lump sum, via a life insurance annuity, or through a retained asset account. Check with the insurer to see which life insurance payout options they offer.

Who pays for life insurance?

During the term, the policyholder makes fixed premium payments in exchange for a guaranteed death benefit. Under a term life policy, coverage ends at the end of the term. However, some insurance companies allow policyholders to extend the coverage to another term or convert it to a permanent policy.

Conclusion

Life insurance is a crucial component of financial planning, offering protection and peace of mind. Understanding policy options, addressing pre-existing conditions, and regular reviews ensure effective coverage. Early planning, consideration of alternatives, and transparent disclosure contribute to a comprehensive life insurance strategy. Consulting with financial experts aids in navigating the complexities, ensuring that policies align with individual needs and provide financial security for the future.